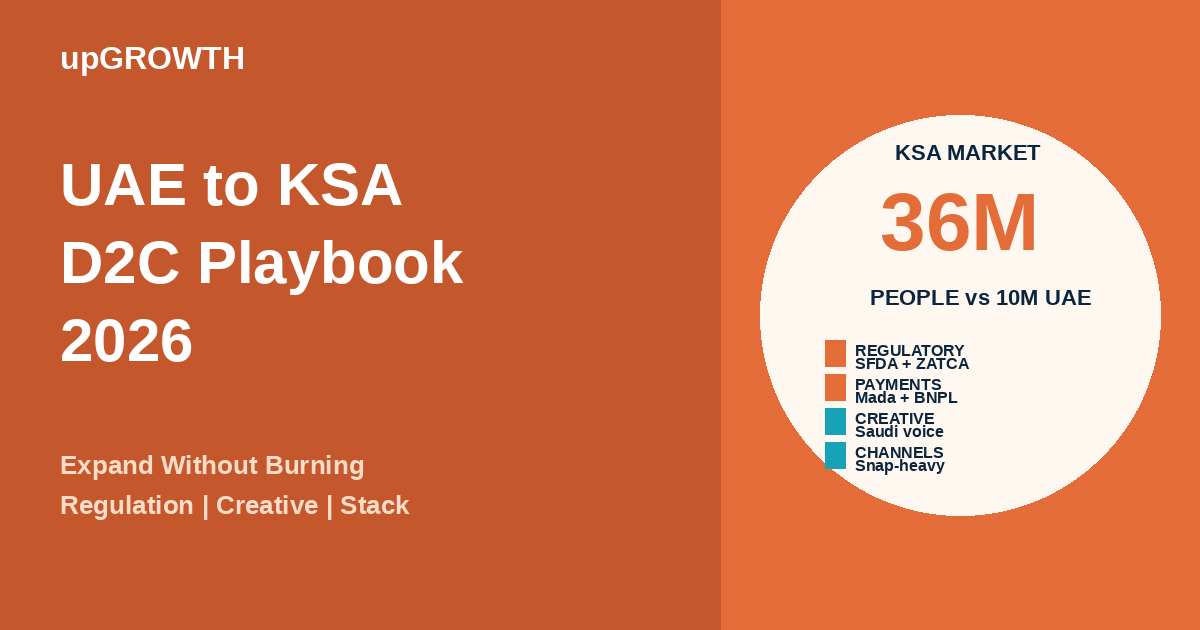

Expanding a D2C brand from UAE to Saudi Arabia is not a simple GCC extension. KSA has different buyer psychology, a larger but less digitally mature population, distinct regulatory friction through SFDA and ZATCA, Saudization hiring pressure on commercial teams, and a creative language that Khaleeji dialect alone does not fully solve. Brands that treat Riyadh as a bigger Dubai burn 6 to 12 months of capital learning the market the hard way. Brands that plan KSA as its own market unlock the largest D2C population in the GCC at 36 million people with median spending power climbing every quarter.

In This Article

Share On:

Every D2C founder who wins in Dubai eventually asks the same question. “How do we expand to Saudi?” The answer most agencies give is some variation of “run the same Meta campaigns with Riyadh geo-targeting and ship via Aramex.” That answer is wrong. It is also the reason most UAE-born D2C brands struggle in Saudi for their first year.

Saudi Arabia is 36 million people against the UAE’s 10 million. The median disposable income is lower but the population curve is younger. The regulatory load is heavier. The logistics network is less dense outside Riyadh, Jeddah, and Dammam. The buyer is more price-conscious on first purchase but more loyal after trust is established. Creative that performs in Dubai often lands flat in Riyadh because the cultural register is different, the humor is different, and the social proof that moves a buyer is different.

At upGrowth Digital, we have helped UAE-based D2C brands enter KSA in categories from beauty to food to homeware. The brands that executed the expansion correctly hit break-even in month 6. The brands that treated Saudi as “UAE plus Riyadh” took 14 to 18 months to find their footing. This playbook is the difference between those two outcomes.

Why UAE Playbooks Do Not Transfer Cleanly to KSA

The first mistake is assuming Saudi is a bigger version of the UAE. The market size is larger, yes, but almost every other variable changes.

Buyer psychology is different. The UAE buyer has been conditioned by a decade of expat-driven D2C experimentation. Average order values are higher. Trust in new brands is built through polished creative, influencer endorsement, and visible social proof. The Saudi buyer is more skeptical on first purchase, values local presence more heavily, and relies on WhatsApp-based customer service and word of mouth far more than the UAE buyer does. A first-time buyer in Jeddah wants to know the product is Saudi-made or Saudi-registered before they trust the brand. That signal barely matters in Dubai.

Demographics skew younger and more mobile-only. Over 63 percent of Saudi Arabia’s population is under 30. Mobile internet penetration is above 98 percent. Desktop browsing is negligible. Snapchat has deeper penetration than in any other GCC market at roughly 90 percent of internet users aged 16-34. TikTok is the fastest-growing platform. Meta is still dominant for purchase-intent campaigns but the creative format that works on Meta in KSA is different from what works in the UAE. Vertical, fast-paced, UGC-led, locally voiced.

Regulatory friction is real. Saudi has three regulatory bodies that D2C brands must respect. SFDA (Saudi Food and Drug Authority) governs food, beverages, cosmetics, and supplements. ZATCA (Zakat, Tax and Customs Authority) governs VAT compliance and e-invoicing through the Fatoora platform. The Ministry of Commerce requires specific product labeling in Arabic for most categories. Compliance is not optional. Non-compliant shipments get held at customs. Non-registered cosmetic products can be removed from platforms by enforcement sweeps.

Logistics density drops outside major cities. Riyadh, Jeddah, and Dammam have same-day or next-day delivery infrastructure through local 3PLs like SMSA, Aramex KSA, and Naqel. Beyond these cities, delivery times extend to 3-5 days and cash on delivery failure rates climb. This matters because COD still accounts for roughly 35-45 percent of D2C transactions in KSA.

Before running a single ad in Saudi, a UAE-born D2C brand must complete this checklist. Skipping items here is what causes the 14-to-18-month delay to profitability.

Legal and regulatory foundation. Decide whether you operate through a KSA entity (Saudi commercial registration) or through a UAE entity with cross-border shipping. Each has tradeoffs. A Saudi entity unlocks local payment processors, faster SFDA registration, and eligibility for local marketplaces like Salla and Zid at better terms. A UAE-based cross-border model is faster to launch but caps your ceiling. Most brands doing more than AED 500K per month in KSA eventually need a local entity.

If you ship food, beverages, supplements, or cosmetics, SFDA product registration is mandatory. Registration takes 4-12 weeks depending on category and complexity. Build this lead time into your launch plan. Non-registered products get stopped at customs.

ZATCA e-invoicing compliance is enforced. If you sell B2C through your own Shopify storefront with local fulfillment, you need Fatoora-compliant invoicing. Work with a Saudi accountant before launch, not after your first ZATCA notice.

Payments and checkout. Saudi buyers expect Mada (the local debit card network), Apple Pay, STC Pay, and Tabby or Tamara for buy-now-pay-later. If your checkout only offers Visa and Mastercard, you will lose 20-35 percent of conversions compared to a checkout that includes Mada and BNPL. Cash on delivery is still expected in roughly 35-45 percent of transactions. Plan for it. Budget for the operational tax of COD.

Logistics partner selection. SMSA Express, Naqel, and Aramex KSA are the dominant local 3PLs. Each has different strengths. SMSA has the deepest last-mile network in Riyadh and Jeddah. Naqel is strong on COD reconciliation. Aramex KSA gives you cross-GCC consolidation if you want to fulfill from a UAE warehouse. For brands under 500 orders per month, cross-border from Dubai is viable. Above that, local warehousing in Riyadh or Dammam becomes a margin decision.

Customer service infrastructure. Saudi buyers use WhatsApp as the default service channel. A WhatsApp Business account with Arabic-fluent agents is not a nice-to-have. It is the single biggest trust signal a new brand can send. Email support is barely used. Phone support is preferred for high-value orders.

Creative Strategy for KSA vs UAE

The creative shift from UAE to KSA is the one most UAE-based brands underestimate. Running the same ad creative with Riyadh geo-targeting produces worse CTRs, lower engagement, and higher CPAs. The reason is that the cultural codes, pacing, and visual language that work on a Dubai audience read as foreign or out of place to a Riyadh or Jeddah buyer.

Dialect and voice. Khaleeji Arabic is the right base register for GCC creative but within Khaleeji there are subregional differences. Saudi buyers respond to creative that uses Saudi-specific expressions, references, and voice talent. If your UAE creative used Emirati voice talent, that registers as “foreign Khaleeji” to a Saudi ear. Local voice talent, local vernacular, and Saudi-specific cultural references move the needle. This is not a theoretical point. We have measured CTR lifts of 40-80 percent on identical creative where the only change was Saudi voice talent over Emirati voice talent.

Platform mix shifts. In the UAE, a 60/30/10 Meta/TikTok/Snapchat split is common. In KSA, the right starting split is closer to 40/30/30 with Snapchat taking a much larger share, particularly for reach in the 16-34 demographic. Snapchat AR lenses are a credible performance channel in KSA in ways that are not true in most other markets.

Visual references. Creative that shows Dubai skyline cues, Palm Jumeirah imagery, or UAE-specific lifestyle references reads as “not for me” to a Saudi buyer. Riyadh skyline, Edge of the World, Jeddah Corniche, and AlUla imagery signal local relevance. Product-on-white static creative can be market-agnostic but lifestyle creative must be locally recontextualized.

The paid media structure for KSA entry has specific sequencing that differs from UAE launch patterns. Running all channels simultaneously from day one wastes budget. The correct sequence builds signal and proof before scaling.

Phase 1 (weeks 1-4): Awareness and creative learning. Run Meta reach campaigns with 4-6 creative variants on minimal budget (roughly AED 15,000 or SAR 15,000 equivalent for the month). Goal is to identify which creative angles resonate with Saudi audiences before scaling. Measure CTR, thumb-stop rate, and hook retention. Kill variants that underperform the market median. Do not worry about CAC in this phase. Worry about creative signal.

Phase 2 (weeks 5-8): Conversion validation. Scale the winning creative variants into conversion campaigns. Add Snapchat and TikTok with the same creative reformatted for each platform. Budget scales to roughly AED 40,000 to 60,000 per month. Goal is to validate that CAC is within the band you can sustain. If CAC is 30-50 percent higher than your UAE CAC, that is normal for market entry. If it is 2x or more, something is wrong with creative, targeting, or landing page.

Phase 3 (weeks 9-16): Scaling and channel expansion. Add Google Shopping, search, and retargeting layers. Build email and WhatsApp remarketing flows. This is where brand search volume starts to appear, which is the clearest signal that the brand is entering Saudi buyer memory. Budget scales to roughly AED 120,000 to 200,000 per month if the unit economics work. If they do not, do not scale. Go back to Phase 2 and fix the creative or the offer.

Phase 4 (months 5-6): Organic and retention layers. Start investing in SEO for Saudi-specific queries, particularly through Arabic content. Build out the WhatsApp broadcast list. Launch a referral or loyalty layer. This is when compounding starts.

Brands that try to run Phase 3 or Phase 4 in month 1 burn 40-60 percent more capital than brands that sequence properly. Patience at launch pays back compounding returns by month 9.

Hiring, Saudization, and Commercial Team Setup

If your KSA expansion involves a local entity, Saudization (also called Nitaqat) becomes a planning constraint. The Ministry of Human Resources requires Saudi national quotas in most commercial roles. The percentage varies by company size and sector. Non-compliance restricts your ability to hire non-Saudis, renew visas, and transact with government entities.

The practical implication for a D2C brand is that your Saudi team cannot be all-expat. Your country manager, customer service lead, and commercial lead should ideally be Saudi nationals. This is both a regulatory fit and a market fit. A Saudi-led team understands the buyer in ways an expat team will not, regardless of how good the expat team is. Hiring quality Saudi talent is competitive and expensive. Budget 30-50 percent more for Saudi commercial hires than equivalent UAE hires for the same role.

Cross-border models (UAE entity shipping into KSA) sidestep Saudization but also cap your brand ceiling. Most brands that plan to exceed AED 1 million per month in Saudi revenue eventually build a local team.

Distribution Partners, Marketplaces, and the Local Platform Question

Pure D2C is harder in Saudi than in the UAE. The buyer habits skew more marketplace-first. Noon, Amazon.sa, Salla, and Zid are not optional channels for most D2C brands. They are discovery engines and trust signals.

Noon and Amazon.sa are marketplace-led distribution. They give you reach and fulfillment infrastructure in exchange for platform fees (12-22 percent depending on category) and margin compression. Most D2C brands treat them as a second channel alongside their own storefront.

Salla and Zid are Saudi-built Shopify competitors. They are the default storefront platforms for Saudi small and mid-size D2C brands. For a UAE-based brand entering Saudi, staying on Shopify is fine if your brand is already established there. Launching a net-new Saudi-focused storefront on Salla or Zid can unlock local payment gateway integration, Mada support, and local SEO advantages.

Tabby and Tamara are not optional. Saudi BNPL penetration is high. Checkout without Tabby or Tamara loses conversions.

UAE to KSA D2C Expansion Strategic Pillars

Expansion Pillar

Key Strategy/Requirement

Expected Outcome/Benchmark

Regulatory

SFDA product registration and ZATCA e-invoicing (Fatoora) compliance.

Q: How much capital do I need to launch a D2C brand in Saudi from a UAE base?

A: A realistic minimum is AED 400,000 to 800,000 for the first 6 months covering inventory positioning, SFDA registration if applicable, paid media launch, Saudi voice creative production, WhatsApp and customer service setup, and a local country manager or consultant. Brands that launch with less than AED 300,000 almost always run out of runway before they find product-market fit in the Saudi buyer context.

Q: Do I need a Saudi entity on day one?

A: No. Most UAE-born D2C brands start cross-border through Aramex KSA or SMSA, fulfill from a Dubai warehouse, and accept the slower delivery times and higher COD failure rates as a tradeoff for speed-to-market. Once monthly Saudi revenue exceeds roughly AED 500,000, the operational and economic case for a local entity becomes clear. At that point the entity unlocks better payment gateway terms, local warehousing, and Saudi tax efficiency.

Q: How is Saudi D2C different from UAE D2C in terms of return rates?

A: Saudi return rates run 10-15 percent for most D2C categories. UAE return rates run 8-12 percent. The gap is driven by higher COD share, longer delivery times outside Riyadh and Jeddah, and slightly higher refusal rates on COD orders. Budget for this in your unit economics.

Q: Which influencer strategy works in Saudi vs UAE?

A: Saudi influencer marketing skews heavier toward Snapchat and Twitter than UAE. Saudi buyers trust micro-influencers with strong WhatsApp community presence over polished Instagram influencers. The average engagement-to-conversion translation is weaker for large Saudi Instagram accounts than for Saudi Snapchat creators with 50,000 to 200,000 followers. Local voice talent and Saudi-accent creators outperform pan-Arab creators in conversion.

Q: How long does SFDA registration take for cosmetics or supplements?

A: For cosmetics, SFDA notification typically takes 4-8 weeks if your product documentation is complete. For supplements and functional food, registration takes 8-16 weeks and often requires GMP certification from your manufacturer. Start this process at least 3 months before your planned Saudi launch date.

Q: Should I translate my UAE creative or produce fresh Saudi creative?

A: Translation alone does not work. At minimum, re-voice your existing creative with Saudi voice talent, reshoot lifestyle scenes with Saudi-relevant locations if you use lifestyle footage, and reshoot UGC with Saudi creators. If budget is constrained, start with re-voicing and add local reshoots as revenue funds them. The budget increment for proper Saudi creative adaptation is typically 30-60 percent of your UAE creative production cost, not 100 percent.

Q: What is the biggest mistake UAE-based D2C brands make when entering KSA?

A: Treating Saudi as “bigger Dubai.” This mistake manifests as running UAE creative with Riyadh geo-targeting, using the same influencer mix, assuming the same AOV and checkout expectations, and under-investing in WhatsApp customer service. Brands that make this mistake typically spend 6-9 months with unprofitable unit economics before they realize the market is fundamentally different and rebuild their approach.

Your Next Move: A Saudi Expansion Strategy That Does Not Burn Runway

Expanding from UAE to Saudi Arabia is the largest single addressable market unlock available to a GCC-born D2C brand. The prize is a 36 million person market with rising disposable income, young demographics, and high digital engagement. The cost of getting it wrong is 12 to 18 months of capital burned on a market you did not plan for.

Most brands do not need more ad budget to win in Saudi. They need a sequenced expansion plan that respects how different the Saudi market actually is. Creative adaptation, regulatory readiness, logistics planning, payment stack, and commercial team build all need to be sequenced correctly or the compounding effect of getting any single element wrong extends your payback period.

If you are a UAE-based D2C brand planning to enter Saudi in the next 6 months, the fastest way to avoid the common mistakes is to build a 90-day expansion sprint with clear milestones on regulatory, logistics, creative, and media readiness before you spend a single riyal on paid acquisition.

This strategy fails because it ignores critical differences in KSA's buyer psychology, regulatory landscape, and media consumption. A campaign that works in the UAE often lands flat in Saudi Arabia because the markets are fundamentally distinct, leading to wasted capital and a timeline of 14 to 18 months just to find footing. Success requires a bespoke strategy that respects these differences from day one. A localized approach acknowledges that the Saudi buyer is more skeptical on first purchase, places a higher value on local presence and word-of-mouth recommendations, and is more price-conscious. Unlike the D2C-acclimated UAE consumer, trust must be earned through culturally resonant signals, not just polished creative. Furthermore, over 63 percent of the KSA population is under 30, with Snapchat penetration at 90 percent, demanding a different creative style than what performs on Meta in Dubai. Discovering how to build this market-specific playbook is key to unlocking growth.

These bodies introduce non-negotiable compliance layers that are more stringent than in the UAE. The SFDA (Saudi Food and Drug Authority) governs product registration for entire categories like cosmetics and food, while ZATCA (Zakat, Tax and Customs Authority) mandates specific e-invoicing through its Fatoora platform. Ignoring these requirements from the start is a recipe for operational failure. Unlike a simple cross-border shipment, entering KSA means adhering to a formal regulatory framework. Key operational hurdles include:

Product Registration: Cosmetics, supplements, and food products must be registered with the SFDA before they can be legally sold and marketed. Non-compliant products risk being seized at customs or removed from sale.

E-invoicing: All transactions must comply with ZATCA's e-invoicing rules, which requires technical integration and specific accounting practices.

Arabic Labeling: The Ministry of Commerce requires detailed product information to be presented in Arabic on the packaging for most consumer goods.

Proactive engagement with these rules prevents your inventory from getting stuck and ensures a smooth path to market.

Raw, authentic user-generated content consistently outperforms polished studio creative in Saudi Arabia, especially on platforms where the under-30 demographic dominates. This is because KSA consumers value authenticity and local social proof more than the high-gloss aesthetic that works with Dubai's expat-heavy audience. You should prioritize creative that feels native to the platform. For TikTok and Snapchat, this means embracing vertical, fast-paced videos that feature local creators and reflect regional humor and dialect. While Meta remains a key channel for purchase intent, even there, UGC-led creative drives better results. The Saudi buyer is more skeptical and looks for signals that a brand understands their culture. Polished ads can feel distant, whereas content from a trusted local voice builds credibility and moves a potential customer from consideration to purchase much more effectively. The full article provides examples of creative that bridges this cultural gap.

The difference is stark, impacting both speed to profitability and overall capital efficiency. Brands that implement a customized KSA strategy typically reach break-even within six months, whereas those that treat Saudi as a larger UAE take 14 to 18 months to find stable footing, burning significant capital in the process. This 12-month gap represents the cost of learning the market the hard way. The successful cohort invests upfront in understanding local nuances. They register products with the SFDA early, establish logistics with local 3PLs like SMSA, and develop culturally specific creative. This preparation allows them to gain traction quickly. In contrast, the struggling cohort spends its first year dealing with held shipments, ineffective ad spend, and high customer service loads from unmet expectations. The financial implication is clear: a customized approach is not a cost but an investment that accelerates your path to capturing the 36 million-person market.

To capture the youth demographic in KSA, you must dominate on Snapchat and TikTok with mobile-first, authentic content. These platforms are not just for awareness; they are primary channels for discovery and validation among Saudi consumers, with Snapchat reaching approximately 90 percent of internet users aged 16 to 34. The content style that works is fast-paced, user-generated, and features local creators who speak the specific dialect and understand the cultural context. Polished, corporate-style video creative often fails to connect. Instead, focus on building social proof through influencer collaborations that feel genuine and running ad formats that mimic organic content. Furthermore, since browsing is almost exclusively mobile, ensuring a seamless checkout experience on a mobile-only journey is critical. Integrating with local payment gateways and offering clear customer support via WhatsApp are essential trust signals for this audience. Gaining early traction with this group is foundational for long-term success.

Achieving breakeven in six months requires a disciplined, front-loaded operational plan focused on compliance, fulfillment, and cultural resonance. Rushing to market without this foundation is what stretches the timeline to over a year. Your first priorities should be:

SFDA Product Registration: Immediately begin the process of registering all your cosmetic products with the Saudi Food and Drug Authority. This is a non-negotiable step for market access. Failure to comply will result in shipments being held indefinitely at customs, halting your entire operation before it starts.

Secure a Local 3PL Partner: Do not rely solely on cross-border shipping from the UAE. Partner with a KSA-based third-party logistics provider like SMSA or Naqel to manage local inventory. This reduces delivery times within major cities and helps manage the complexities of cash on delivery (COD).

Develop Locally Resonant Creative: Hire local Saudi creators or a specialized agency to produce ad content for TikTok and Snapchat. Your Dubai-centric creative will not work. Focus on UGC-style videos that use local humor, dialects, and influencers to build immediate trust.

Executing these steps correctly from the outset is the core difference between rapid growth and a costly stall.

The most frequent and costly mistake is underestimating the challenges of cash on delivery (COD) outside of KSA's three main cities. While COD is declining, it remains a significant payment method, and failure rates climb dramatically in less dense areas, erasing profit margins. Brands relying on cross-border shippers like Aramex without a local presence see higher return-to-origin rates due to longer delivery windows and coordination issues. A dedicated local 3PL partner is the solution. By holding inventory within KSA and using a provider like SMSA or Naqel, you can significantly reduce delivery times from 5-7 days to 1-3 days. This shorter window dramatically lowers the rate of COD refusals, as the purchase is still top-of-mind for the customer. These local partners also have better on-the-ground communication systems to coordinate deliveries, further increasing the success rate. This single operational choice directly impacts your profitability and customer experience.

Brands must evolve their strategy from pure customer acquisition in major cities to building a durable, nationwide presence. This requires shifting focus towards customer retention and logistical excellence across the entire kingdom, as a significant portion of the 36 million-person market lies outside the main hubs. Your two-year plan should incorporate investments in infrastructure and community-building that create a local feel. Key strategic adjustments include establishing a more distributed logistics network, possibly with fulfillment nodes in secondary cities to ensure 2-day delivery becomes the standard. You should also invest heavily in Arabic-first customer support, particularly through WhatsApp, to build trust and handle inquiries from a diverse customer base. Finally, marketing efforts must move beyond performance ads to cultivating brand loyalty through community engagement, localized content, and loyalty programs that resonate with Saudi cultural values. Winning the next phase of KSA e-commerce means being seen as a local brand, not a foreign one.

In Saudi Arabia, influencer marketing must be rooted in genuine trust and cultural authenticity, not just reach and polished endorsements. Unlike the UAE where high-profile influencers can drive sales through aspirational content, Saudi consumers are more moved by relatable creators who they feel genuinely believe in a product. This means your strategy should prioritize micro- and mid-tier influencers with deep, authentic connections to their audience. The key is to find voices that can create user-generated-style content that feels more like a recommendation from a friend than a paid advertisement. For example, a campaign with a local Riyadh-based food blogger who unboxes and uses a homeware product in a realistic setting will outperform a glossy post from a top-tier fashion influencer. Success depends on building long-term relationships with a portfolio of trusted local creators, a lesson brands like those guided by upGrowth Digital learn early.

The primary cause is a failure to appreciate the deep cultural and linguistic nuances that differentiate Saudi consumers from the broader Khaleeji audience. Simply translating an ad or using a generic Gulf dialect is insufficient; the humor, social cues, and visual language are distinct. Brands fail when they assume creative that works for an expat-heavy audience in Dubai will connect in Riyadh. To solve this, you must integrate local Saudi talent directly into your creative process. This is not about simple consultation; it is about co-creation. The most effective method is to build a roster of Saudi UGC creators, scriptwriters, and videographers. Let them lead the ideation for platforms like TikTok and Snapchat. This ensures the output is not just 'localized' but culturally native. Testing different creative angles from these local creators will quickly reveal what drives both engagement and, more importantly, conversions in this unique market.

A robust, WhatsApp-centric customer service system is a critical trust signal for the Saudi buyer, who is often more skeptical on first purchase. It provides the direct, personal interaction they value and can be a key differentiator. A practical implementation plan involves three steps.

Set Up a KSA-Specific Number: Use a local Saudi phone number for your WhatsApp Business account. This simple detail signals a local presence and commitment to the market, which is far more reassuring than an international number.

Staff with Native Arabic Speakers: Hire customer service agents who are native Saudi or fluent in the specific local dialect. They can handle inquiries about products, delivery from 3PLs like Naqel, and payment with cultural nuance, building rapport effectively.

Integrate Pre- and Post-Purchase Support: Use WhatsApp not just for troubleshooting but also for pre-sale questions, which can directly lead to conversions. Proactively send order updates and delivery notifications through the platform to create a seamless experience.

This high-touch communication strategy addresses the Saudi consumer's need for assurance and can significantly boost both initial sales and long-term loyalty.

To build a lasting brand in Saudi Arabia, you must invest in deep operational and cultural integration. Simple translation and cross-border shipping will not be defensible as the market gets more competitive; long-term success requires being perceived as a local entity. The most critical investments are in physical presence, local team building, and authentic brand partnerships. This means moving beyond a single 3PL partner like Aramex KSA to establishing your own fulfillment capabilities or multi-node warehousing to guarantee next-day delivery nationwide. It also involves hiring a local Saudi marketing and commercial team, not just remote managers, to ensure your strategy is always aligned with market pulse. Finally, forge partnerships with Saudi-owned businesses, sponsor local events, and create content that celebrates Saudi culture. These investments signal a commitment to the market that builds a moat around your brand that competitors cannot easily cross.

Amol has helped catalyse business growth with his strategic & data-driven methodologies. With a decade of experience in the field of marketing, he has donned multiple hats, from channel optimization, data analytics and creative brand positioning to growth engineering and sales.

Growth Strategy and Planning

Growth Strategy and Planning Inbound Growth

Inbound Growth Growth Hacking

Growth Hacking Fractional CMO

Fractional CMO Search Engine Optimization

Search Engine Optimization Paid and Performance Marketing

Paid and Performance Marketing Social Media Marketing

Social Media Marketing Demand Generation

Demand Generation AI-Driven Growth Strategy

AI-Driven Growth Strategy AI-Native Workflow Automation

AI-Native Workflow Automation Generative Engine Optimization

Generative Engine Optimization Grove — AI Growth Strategist

Grove — AI Growth Strategist

AI Automation

AI Automation Framework

Framework Case Study

Case Study Tools

Tools Growth Tools

Growth Tools Decision Tree

Decision Tree Compare

Compare Custom GPT's

Custom GPT's Guides

Guides Offer

Offer Webstories

Webstories Quizzes

Quizzes Blog

Blog AI-powered Apps

AI-powered Apps Social Media Tools

Social Media Tools Agency Fit Score

Agency Fit Score